Director, Head of Reinstatement Cost Assessments

James Key

Insights

17 Jun 2026

Recent industry data highlights a persistent challenge: underinsurance remains widespread across commercial property portfolios. An Insurance Times article suggested that nearly half of assets are underinsured, with an average shortfall of around 40%.

While market conditions may offer temporary relief, the underlying issue is more structural. Too often, building assessments are not carried out regularly – and when they are, they are not always consistent or sufficiently robust.

The Problem with Inconsistent Approaches

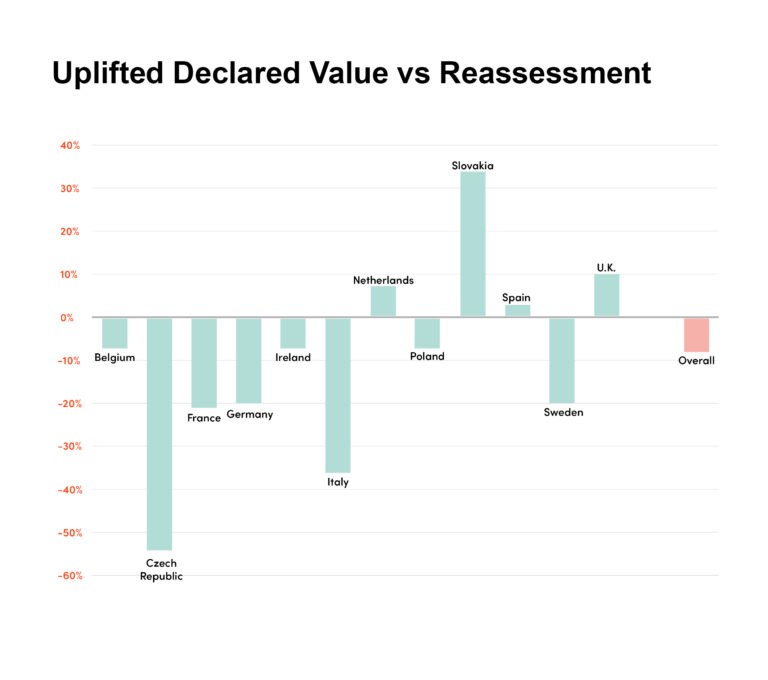

For many multi-site or international portfolios, inconsistency is a defining challenge. Different methodologies adopted by local providers can lead to significant variations in declared values, making it difficult to maintain a clear and reliable view of exposure.

If we look at a typical example of a pan-European logistics portfolio we reassessed over several years. Comparison of historic declared values against detailed reassessments showed wide variance across countries, with a greater proportion of assets falling below the required level of cover.

The overall result was an 8% underinsurance position and a significant impact on the premium.

This is not simply a valuation issue; it is a data issue.

Why Better Data Matters

The traditional approach to cost assessment – applying benchmark rebuild rates to floor areas – relies heavily on assumptions and often incomplete inputs.

Yet buildings are complex, and their costs are not uniform. The difference between a shopping centre mall and a car park, or between a premium hotel and a budget roadside asset, can be substantial.

A more accurate approach relies on detailed measurement, structured data collection, and elemental costing -building up a unique cost model that reflects the actual characteristics of each asset.

Crucially, this level of detail does more than improve accuracy. It enables:

- Better risk assessment

- Greater transparency for insurers

- More informed decision-making across the portfolio

And ultimately, it demonstrates that a portfolio is being actively and professionally managed – often resulting in more favourable insurance outcomes.

The Role of Consistency

Even the most accurate dataset can quickly lose relevance if it is not maintained. Insurance values are, by nature, a point-in-time view – and without regular reassessment, the gap between declared value and true exposure can widen rapidly.

Consistency, therefore, is not just about methodology – it is about continuity.

A consistent, data-led approach ensures that:

- Assessments are comparable across assets and geographies

- Changes in cost and risk are tracked over time

- Decisions are based on a single, reliable source of truth

Introducing Hollis Engage

To address these challenges, Hollis has developed a new approach to managing insurance data through Hollis Engage – a digital platform designed to bring consistency, transparency, and control to RCA portfolios.

Hollis Engage hosts all RCA reports in one place, allowing users to:

- Access assessments instantly

- Monitor when reassessments are due via a portfolio dashboard

- Work with fully interactive data rather than static PDF outputs

Importantly, the platform moves beyond traditional reporting. All assessments are maintained as live data, ensuring consistency across the portfolio regardless of when individual assessments were originally prepared.

Users can access up-to-date declared values at any time—supporting both internal decision-making and collaboration with brokers and insurers.

From Data to Better Outcomes

By embedding consistent, high-quality data into the assessment process, Hollis Engage transforms how insurance is managed.

This is not just about operational efficiency. It is about:

- Reducing exposure to underinsurance

- Ensuring coverage reflects real-world costs

- Building resilience across property portfolios

Ultimately, better data leads to better decisions – and better outcomes for both owners and insurers.